AI Doom and Gloom Predictions

Every few months, a new blog predicts the end of work as we know it. “Unemployment surging past ten percent. Markets down forty.” AI rendering entire professions obsolete before the decade is out. The charts are alarming, the language is urgent, and the assumptions tend to fall apart pretty quickly if you actually stop and poke at them.

For example, unemployment isn't just a count of lost jobs. It's a ratio, people out of work divided by the number of people willing and able to work. With immigration tightening and birth rates sitting below replacement level, the labor pool is already shrinking on its own. AI displacing roles in that environment might not produce the crises these reports are warning about. It might barely register. In some sectors, it might actually solve a problem we have yet to address.

Productivity Boom?

For years, the standard critique of AI hype has been simple: where are the productivity gains? The macro data wasn't moving. Billions poured into infrastructure, millions of users, and the output numbers barely budged.

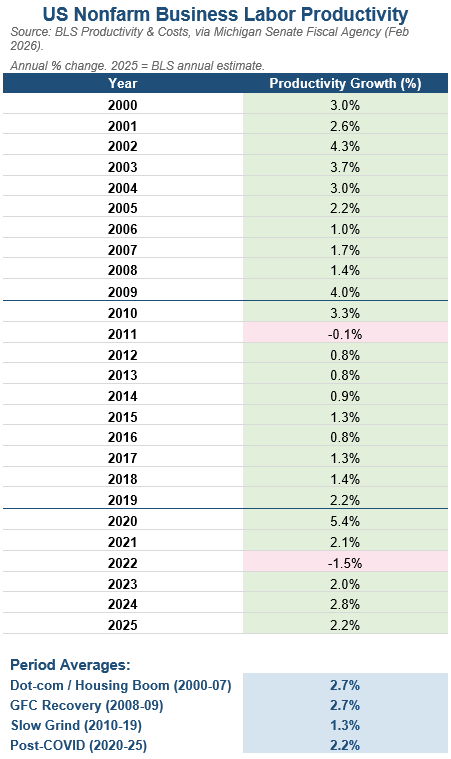

Looking at BLS non-farm business productivity data through 2025, something is finally showing up. After a dismal 2022 when productivity fell by 1.5%, the numbers have accelerated meaningfully. 2023 came in at 2.0% growth. 2024 stepped up to 2.8%. And for full-year 2025, we're at 2.2%, with some notably strong quarters (Q3 hit 4.9% annualized). That three-year stretch is the best sustained run since the mid-2000s.

The 2000s averaged roughly 2.7% productivity growth per year. That was a period of massive capital expenditure (sound familiar?), broadband rollout, and enterprise software adoption that we now regard as relatively ordinary tech diffusion. The 2010s, the decade of smartphones, social media, and cloud computing, averaged somewhere between 0.8% and 1.2% depending on the measure. The Conference Board puts it at 0.8%. BLS non-farm business data comes in a bit higher. Either way, it was the weakest sustained productivity stretch in modern American economic history.

The gap between what the most sophisticated users are experiencing and what the aggregate data shows is still enormous. If you're an engineer at Amazon, Google, or Microsoft, you're living inside the most productive edge of that curve. A full day's work compressed into hours is a real experience for some people right now. But that experience hasn't yet propagated through the broader economy in a way that justifies the more dramatic predictions being made.

Underneath all the noise, something genuinely significant is happening. And as engineers at some of the most AI-exposed companies in the world, you're closer to it than almost anyone.

When the Ladder Gets Pulled Up

Dario Amodei, CEO of Anthropic, has said publicly that AI will eliminate fifty percent of entry-level white-collar jobs within one to five years. Plenty of people in the industry think he's being conservative. And we're already seeing the early signals as recent college graduates are struggling to land entry-level positions at a rate that stands out even against a broader softening job market.

These aren't just numbers. They represent the disappearance of the roles that used to be the starting point for an engineering career. Junior developer positions. Entry-level analyst work. The jobs where you learned by doing and slowly built the experience that made you valuable.

Here's the structural problem nobody is talking about loudly enough: you cannot build senior engineers without junior engineers first. When the bottom rungs of the ladder disappear, the entire climb breaks down. Employers may be winning on efficiency today, but they could be quietly starving the talent pipeline they'll desperately need a decade from now.

It's Happening in Real Time

In February 2026, engineer and entrepreneur Matt Shumer published an essay called “Something Big Is Happening”. It's worth reading if you haven't. He describes what programmers are quietly experiencing right now.

Over a surprisingly short window of time, AI tools went from saving him a few minutes of work to replacing nearly a full day's worth of coding output, with the number of corrections he had to make dropping from frequent to almost zero. He doesn't really need to code in the traditional sense anymore. The AI handles it.

For a profession that assumed it was largely disruption-proof (engineers build the tools that displace other people, after all) that's a striking data point. Coding turns out to be rule-based enough for AI to do at a high level. The irony isn't lost on anyone: the tech industry spent years accelerating AI development, and AI is now accelerating the displacement of the people who built it.

Real Consequences Based On Guesses

Reports like Citrini Research's 2028 Global Intelligence Crisis paint a dramatic picture — double-digit unemployment, market crashes, widespread collapse of knowledge work. It makes for gripping reading. But some of the underlying logic deserves scrutiny.

Beyond the population math we mentioned earlier, there's a sector problem. AI doesn't disrupt everything equally. Agriculture, skilled trades, aviation, healthcare — these remain largely resistant to near-term automation. Someone still needs to harvest the strawberries, fly the planes, and staff the hospitals. The question isn't whether those jobs exist. It's whether displaced white-collar workers are willing or able to take them. And honestly? History says that transition is slow, painful, and full of friction. A laid-off software engineer isn't going to cheerfully retrain for agricultural work, and even if they wanted to, the pay and career trajectory look nothing like what they left behind.

There's also the circular economy problem that tends to get buried in these reports. Think about what happens when a company like Salesforce starts shedding headcount at scale. Their revenue drops. Their ad budget shrinks. The broadcasters who relied on that ad spend feel it. The employees who were laid off stop spending. The restaurants, retailers, and service businesses near their offices notice. One domino hits another. The efficiency gains that looked so clean on a spreadsheet start looking messier when you trace them through the real economy.

The Monetization Problem Nobody Has Solved

Here's something worth watching closely from an investment standpoint: the economics of AI at scale are still deeply unresolved.

The infrastructure buildout for large language models runs into the hundreds of billions of dollars. Current subscription pricing doesn't come anywhere close to covering those costs. If platforms raise prices significantly to break even, most users will drift back to free alternatives. If they layer in advertising to compensate, they undermine the core value proposition that made people switch in the first place.

The most credible near-term path to profitability is enterprise cost savings — companies replacing workforce overhead with AI licensing fees. But that's essentially a one-time harvest. You can only cut headcount so many times before you've cut as deep as you can go. And if enough companies do it simultaneously, the consumer spending, tax revenues, and economic velocity that sustain everything else start to erode.

The post-scarcity fantasy — the idea floated by people like Elon Musk that AI could eventually make money itself irrelevant — runs into an even more basic problem. Scarcity doesn't disappear just because labor does. A plane to Hawaii still has a finite number of seats. A beachfront property still has a finite amount of coastline. You need some mechanism to allocate finite resources, whether that's money, credits, or a queue. Price is just a signal. Remove it and you still have the same underlying problem.

What History Tells Us

We've seen technology disrupt industries before. Coal miners didn't lose their jobs overnight when natural gas and renewables started taking market share. Those transitions played out over decades, which gave communities some time to absorb the shock.

The concern this time is speed and breadth. AI isn't targeting one industry or one region. It's compressing what might otherwise be a multi-decade transition into potentially just a few years, across virtually every knowledge-work sector at once. And unlike coal, where displaced workers were concentrated in specific regions, this disruption is centered in San Francisco, Seattle, and other high-earning, high-spending metros.

The jobs that are disappearing first aren't the worst jobs, either. They're the entry points. And that matters, because it breaks the mechanism by which industries develop their next generation of talent.

What This Means for You

We're not writing this to alarm you. We're writing it because the people best positioned to navigate this moment are the ones who see it clearly and plan for it deliberately.

Income diversification matters more than it used to. Depending entirely on a single employer carries more risk than it did five years ago. Skills that complement AI rather than compete with it are worth developing now, and that development has real financial value. Your equity concentration in employer stock deserves a fresh look, particularly if your company's growth story is built on AI-driven headcount reduction. And your long-term assumptions about income trajectory may be due for a realistic update.

The disruption is real. The timeline is genuinely uncertain. But professionals who approach this with clear eyes and a solid financial plan will be far better positioned than those who don't.

Disclosures

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

This document is for your private and confidential use only and not intended for broad usage or dissemination.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of CWA strategies are disclosed in the publicly available Form ADV Part 2A.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. You cannot invest directly in an Index.

Past performance shown is not indicative of future results, which could differ substantially.

Consilio Wealth Advisors, LLC (“CWA”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where CWA and its representatives are properly licensed or exempt from licensure.