Breaking Down Inflation Readings

There are two types of inflation measurements - headline and core. Headline inflation measures everything from furniture, cars, food, gas, etc. Everything that has a price, gets counted. Core inflation measures everything except for food and gas. Why strip out food and gas since everyone consumes food and gas? Regardless of what the Fed does with interest rates, they cannot change demand for food or gas. People are going to consume it, no matter how expensive food and gas get.

The last time we posted about inflation, it was relatively tame at 7%. Seven months later, CPI is coming in at 8.6%. While it isn’t rising as fast, it is still concerningly high. Fuel and airline prices led a broad increase of inflation across nearly all categories. The biggest shift to the market, since our last post, was the Ukraine/Russia war where Russia is a significant supplier of oil. The response to Russian aggression were sanctions, reducing global supply of oil, while simultaneously demand has rebounded.

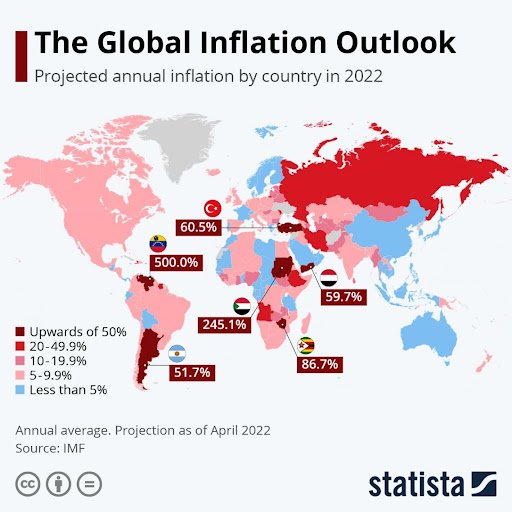

High inflation is not a US problem. On the map below, pink is bad. Red is really bad. Most of the globe is now pink or red.

The concept of “revenge spending” is where people are going to spend because they are sick of being held up in their homes for two years. Retail therapy kept consumers satiated to where retailers could not keep up with demand. As a result, the retailers overordered assuming demand would continue to grow. Now nearly all retail businesses are sitting on excess inventory.

“Revenge spending” has shifted to services, as most of the world has essentially reopened. The demand for airlines, hotels, and rental cars are increasing prices in these categories. As with every other business that did everything to reduce costs, airlines and hotels shed staff, and rental companies shed their fleets. All to now run into pilot shortages, staff shortages, and car shortages.

It’s also the cost of fuel that has the broad effect of prices going up. Hauling tomatoes across the country requires fuel. The oil cartel and producers are reluctant to increase production at the risk of oversupplying the market.

Will it normalize?

As of this article, the Fed has raised rates three times (possibly too slow for some) and will raise rates at least another nine times for the rest of the year. A lot can happen between now and the end of the year, so the Fed can and will alter its course if something changes.

Spending can naturally come down because high prices are destroying budgets. Not everyone is a revenge spender and some spending is coming down. The retailers with too much inventory need to start discounting and cancel orders to ensure they have enough space for other products. This could have a deflationary effect because prices will come down.

Oil supply will need to improve. Whether Ukraine/Russia comes to a resolution, the sanctions most likely will stay in place for the foreseeable future. OPEC and US refiners would need to significantly increase production.

A recession could be the medicine needed. The demand side would need to erode below an already low supply constraint. Bottom line, spending needs to come down while supply needs to continue to improve.

Disclosures

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Consilio Wealth Advisors, LLC (“CWA”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where CWA and its representatives are properly licensed or exempt from licensure.