Q2 2026 Market Commentary: Fire, Oil, and a Market Caught in the Crossfire

This information is meant to be a commentary regarding Consilio Wealth Advisors’ views on the relative attractiveness of different areas of the market, contrasted with our current asset allocation strategy for the near term, 12–18 months. These views are always made in the context of a well-diversified portfolio and are not meant to be a recommendation to buy into or sell out of a particular area of the market. These views can and will change as new information becomes available.

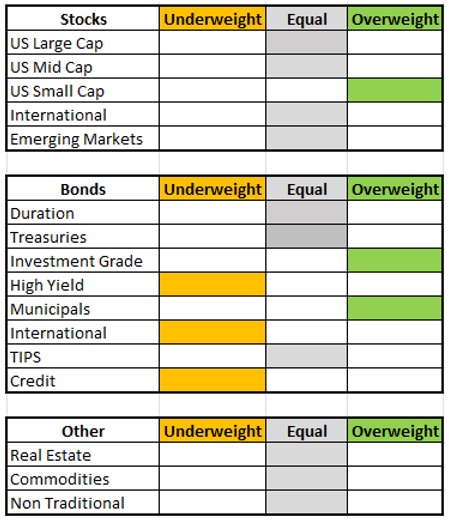

Our Current Positioning

Below is our near-term asset allocation view for the next 12–18 months. The commentary that follows explains the thinking behind these weights.

Views reflect Consilio Wealth Advisors’ near-term (12–18 month) positioning as of Q2 2026. Subject to change as conditions evolve.

Quarter in Review

The story of Q1 2026 can be told in one sentence: the U.S. and Israel launched joint strikes on Iran on February 28, and almost everything that happened to markets afterward was downstream of that decision.

The strike, codenamed “Operation Epic Fury,” sent energy markets into their most violent convulsion since the 1970s oil embargo. The Strait of Hormuz, the narrow chokepoint through which roughly one-fifth of global oil supply travels daily, was effectively closed to commercial shipping. The International Energy Agency called it the greatest global energy security challenge in history. That is not hyperbole.

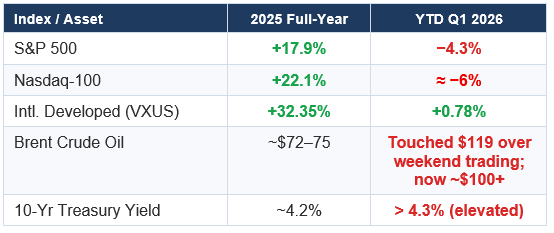

Before the strikes, the S&P 500 had started 2026 mildly, already contending with sticky inflation and a new Fed chair nomination. After February 28, it accelerated its slide. As of late March, the S&P 500 sits roughly 4.3% below where it started the year, while the Nasdaq-100 has shed about 5%. For an index that many Wall Street strategists predicted would be up 10% by year-end, Q1 has been a cold bucket of water.

“The last time we had this much Wall Street consensus on a market outcome, it was heading into 2023 — and every forecast was negative. 2023 finished up 26%.”

That note of humility from our last commentary is even more relevant today. The Iran war was not priced in. Nobody’s year-end S&P target accounted for Brent crude touching $119 a barrel over weekend trading, tanker traffic through Hormuz grinding to a near halt, or Qatar declaring force majeure on liquefied natural gas exports.

The Iran War and the Energy Shock

Here is the uncomfortable arithmetic of the Strait of Hormuz: more than 20 million barrels of oil per day pass through it. When that flow slows to a trickle, Gulf producers including Saudi Arabia, Kuwait, Iraq, and the UAE run out of storage capacity and are forced to cut output. Oil that has nowhere to go cannot be sold. The result is a physical supply crunch, not the financial or sanctions-driven kind the world saw after Russia’s 2022 invasion of Ukraine.

The Russia-Ukraine oil shock was ultimately absorbed through rerouting and substitution. Hormuz does not work that way. Alternative pipeline routes through Saudi Arabia and the UAE can handle, at most, 4.7 million barrels per day, a fraction of the usual flow. You cannot easily reroute 20 million barrels.

Brent crude touched $119 a barrel over weekend trading, close to its all-time high of $147 in July 2008, before settling back near $100 as of late March, still 17–25% above pre-war prices. Every 10% rise in oil prices corresponds historically to about 0.4% higher inflation and 0.15% slower economic growth, per IMF analysis. Do the math on a 25% move, and you see why stagflation, the toxic combination of rising inflation and slowing economic growth, has re-entered the financial lexicon.

What This Means for Your Budget

National average gas price hit $3.41/gallon by early March, up $0.43 in a single week.

LNG disruptions (Qatar declared force majeure) are pushing natural gas and heating costs higher.

Fertilizer prices may roughly double from 2024 levels; food prices are expected to follow upward, particularly for wheat, rice, and corn, as the Gulf accounts for roughly 45% of global sulfur supply used in fertilizer production.

Defense and energy stocks (Exxon, Chevron, Northrop, Lockheed) rose sharply on the news. Not all portfolios lost ground.

Powell’s pushback on “stagflation” is technically accurate. Unemployment is not in double digits, and inflation is not running at 8–10%. But a milder version of the same dynamic, with inflation drifting toward 3–4% while GDP growth decelerates and job creation softens, is a real and present risk. The Fed acknowledged as much in its updated projections: PCE inflation now forecast at 2.7% for 2026, up from earlier estimates, while growth is expected to hold at 2.4%.

The February jobs report already showed a loss of 92,000 positions. Winter weather may be part of the story; the January figure of +126,000 nearly cancels it out. But the trend is worth watching. The white-collar employment slowdown, visible in layoff announcements throughout late 2025 and early 2026, has not fully shown up in aggregate numbers yet.

The Fed: Stuck Between a Rock and a Hard Place

Heading into 2026, markets had priced in two rate cuts. After the Iran war, that expectation has collapsed to one, or possibly zero, depending on which market you consult. The CME FedWatch tool currently implies no cut until mid-2027.

The Fed is in the classic supply-shock bind: inflation is rising from an external cost-push (oil), while demand is at risk of weakening simultaneously. Cutting rates to support growth would risk re-igniting inflation. Holding rates or hiking to fight inflation could tip an already-softening jobs market into something worse.

Powell, for his part, has reiterated that the Fed’s framework remains data dependent. His term expires in May 2026, and Kevin Warsh, Trump’s nominee, will inherit this environment. The transition itself adds policy uncertainty at precisely the wrong moment. A new chair typically needs months to build consensus among the FOMC, and that adjustment period could make the committee more cautious, not less.

Our read: rates stay at 3.5–3.75% through at least mid-year. If oil prices normalize, which would require either a genuine ceasefire or a large coordinated strategic petroleum reserve release, the Fed might find a window for one cut in Q4. If oil stays elevated, that window closes.

The International Reversal Continues

If there is a silver lining to Q1’s turbulence, it is for investors who took our repeated suggestion to not sleep on international diversification. As of late March, international developed-market stocks (proxied by the Vanguard VXUS ETF) are up approximately 0.78% year-to-date, modestly positive compared to the S&P 500’s 4% decline.

Bank of America Research has called 2026 a “new world order” for international equity investors, with data showing four times as much capital flowing into international developed-market funds as U.S. stock funds, roughly $104 billion versus $25 billion. That flow hasn’t fully translated to price yet, but the relative resilience (VXUS roughly flat while the S&P falls 4%) is meaningful. A weaker U.S. dollar, which fell about 9.4% in 2025 on a trade-weighted basis, continues to amplify returns for U.S.-based investors in international assets.

We have been making this point for several quarters: international stocks trade at steep discounts to U.S. equities, roughly 33–38% below historical relative P/E averages for developed and emerging markets, respectively. Valuation is not a catalyst, but combined with dollar weakness and massive capital inflows, it is a tailwind worth owning.

The K-Shape Gets an Oil Tax

In our last commentary, we described the K-shaped economy, where the upper arm (higher-income households, services sector) prospered while the lower arm struggled with costs and weak job growth in manufacturing and goods. The Iran war energy shock is essentially a regressive tax applied to both arms of the K, hitting the lower arm harder.

Higher-income households allocate a much smaller share of their budgets to energy. Rising gas prices, higher utility bills, and more expensive food are a nuisance for them; for lower-income households, these are existential budget pressures. Consumers were feeling better in February than at any point in recent months, and then the war started.

The services sector, which had been the engine of U.S. economic resilience (PMI comfortably above 50), is more insulated from energy costs than manufacturing. But sustained high oil prices eventually bleed into transportation and logistics, raising costs across the board. Manufacturing PMI, already in contraction territory, could deteriorate further.

Government Dysfunction, Grounded at the Gate

While the Iran war dominates headlines, a quieter domestic crisis has been unfolding at airport security lines across the country. DHS funding lapsed in mid-February after Congress deadlocked over immigration enforcement reforms, triggering a partial government shutdown now in its fifth week. The agency that oversees TSA has been operating without a full appropriation, and its 50,000 security officers have been working without their full paychecks.

The results are visible to anyone who flew over spring break. Callout rates spiked above 10% nationally on some days, against a historical baseline of under 2%. At Houston’s William P. Hobby Airport, more than half of scheduled TSA workers called out on a single day. Over 400 officers have quit outright since the shutdown began, unable to afford gas, childcare, food, or rent on missed or partial paychecks. Three-hour security lines at Hartsfield-Jackson, JFK, and Bush Intercontinental have caused passengers to miss flights. At New Orleans, the security line snaked through a parking garage, circling seven times before reaching the terminal entrance.

The administration’s response, deploying ICE officers to assist at airports, drew immediate pushback from both travelers (who reported the agents provided little practical help) and state officials who questioned sending immigration enforcement personnel to perform screening functions they are not trained for. Acting Deputy TSA Administrator Adam Stahl warned that smaller airports could face outright closure if callout rates continue rising.

This is the K-shape in its most literal form. TSA officers, essential workers earning modest salaries, are being asked to screen record spring break travel volumes while simultaneously navigating eviction notices and overdrawn bank accounts. Airline CEOs from American, Delta, Southwest, and JetBlue sent a joint letter to Congress urging a resolution, calling it “difficult, if not impossible, to put food on the table, put gas in the car, and pay rent when you are not getting paid.”

The economic read-through is real. Airlines were projecting a record spring travel season with 171 million passengers over two months, up 4% year-over-year. That demand is colliding with a staffing crisis on the ground. Higher airfares due to fuel costs from the Iran shock are already dampening discretionary travel. Add multi-hour security lines and the travel and leisure sector, one of the stronger corners of the services economy, faces a rough quarter. The previous government shutdown, a 43-day standoff last fall, ended only after the FAA ordered a 10% flight cut at major airports and disruptions became politically untenable. We may be approaching that threshold again.

A Closer Look at Private Credit

Private credit, a $1.8 trillion market where asset managers lend directly to businesses outside of traditional bank channels, has been a popular allocation in recent years, offering floating-rate income and diversification away from volatile public bonds. That thesis remains broadly intact, but there are pockets worth monitoring carefully in the current environment.

Two forces are creating friction. First, corporate borrowers spent 2025 expecting rate cuts that didn’t materialize, deferring refinancing decisions. Now roughly $1.35 trillion in non-financial corporate debt is maturing in 2026 and needs to be rolled over at rates meaningfully higher than when the debt was originally issued. Second, the energy shock has put additional pressure on mid-market borrowers in energy-intensive industries like transportation, logistics, and manufacturing. Business Development Companies (BDCs), publicly traded firms that lend directly to small and mid-sized businesses like a bank but without the regulatory oversight, are beginning to report some elevated stress among these borrowers.

Credit spreads reflect the increased caution. Spreads are the extra interest rate that investors demand to hold corporate debt instead of “risk-free” Treasuries, and they have widened, meaning the market is charging companies more to borrow. Investment-grade companies are now paying roughly 1.2 percentage points above Treasuries, while high-yield borrowers are paying nearly 4.7 percentage points above. Some private credit fund managers have introduced redemption limits as a precautionary measure given the uncertainty.

The key distinction is quality. Well-capitalized, investment-grade borrowers are navigating this environment without major difficulty. The stress is more concentrated in highly leveraged mid-market companies with thin margins, particularly those exposed to rising energy and transportation costs. For clients with private credit allocations, the focus should be on understanding the underlying borrower quality and industry mix. This is a moment for careful monitoring, not alarm.

The AI Spending Question: Build It, and They Will Come?

The other storyline quietly reshaping markets is the scale and scrutiny of AI datacenter spending. The five largest U.S. hyperscalers (Amazon, Microsoft, Alphabet, Meta, Oracle) are on track to spend over $600 billion in 2026, roughly 75% of which is directed at AI infrastructure. That number is six times the 2022 level. It is comparable to the annual GDP of Sweden.

To fund this, the hyperscalers are increasingly tapping debt markets. Capital intensity has reached 45–57% of revenue at some companies, historically unthinkable levels. Aggregate spending now exceeds projected free cash flow for the group, meaning external financing is no longer optional. Over $75 billion in AI-linked corporate bonds were issued in just a two-month window in early 2026.

The bull case is straightforward: every hyperscaler reports that demand is supply-constrained, not demand-constrained. Microsoft has an $80 billion Azure backlog it cannot fill due to power constraints. Alphabet’s cloud backlog surged 55% sequentially. If that demand is real, today’s spending will look visionary in retrospect, the fiber optic cables of the 2030s.

The bear case is equally clear: ROI has not been proven at this scale. Software stocks collapsed nearly 30% between October 2025 and February 2026, partly on concerns that AI is disrupting the very SaaS models that private equity and private credit had been financing. S&P Global has warned that “debt-funded expansion” of datacenters is outpacing equity contributions. Goldman Sachs noted that the timing of any slowdown in spending growth poses a real valuation risk to AI infrastructure stocks, which ran far ahead of actual earnings growth.

Our take: the AI basket is still worth owning broadly rather than through individual picks, but the easy money phase is over. The market is no longer willing to pay unlimited multiples for companies spending furiously with uncertain payoff timelines. Energy constraints are a real bottleneck, and the Iran war only makes this worse as helium and rare materials critical to chip manufacturing are also disrupted via Hormuz. Watch the hyperscaler earnings calls closely this quarter: the question is no longer whether they will spend, but whether they can demonstrate revenue conversion from what they have already built.

Looking Ahead to Q2 and Beyond

The single most important variable for the rest of 2026 is the Iran war’s duration and trajectory. History suggests geopolitical shocks are often short-lived in their market impact. After both Gulf Wars, equity markets posted double-digit gains three to six months after conflict onset, with the defense sector tending to lead. But this conflict has a structural difference: a physical chokepoint, not just financial disruption.

Morgan Stanley’s analysis puts it plainly: the key risk is duration. A swift resolution through ceasefire, diplomatic breakthrough, or military decisiveness would allow energy prices to normalize, the Fed to cut, and markets to recover. A prolonged conflict where Hormuz remains effectively closed for months would be a different and more painful story.

Earnings growth of ~12.5% projected for Q1 2026 remains healthy, and the forward P/E of 20.3x, while above the 10-year average of 18.9x, has compressed from 22x at year-end. The market has done some of the work. But until the energy picture clarifies, upside is capped. Within fixed income, with rates on hold and the yield curve elevated, investment-grade credit and municipals offer relatively attractive risk-adjusted income, consistent with the overweights reflected in our positioning above. High-yield and international bonds face headwinds from the energy shock and dollar volatility. Long-term investors should resist the urge to make dramatic allocation shifts based on headlines.

“The Strait of Hormuz is a physical chokepoint, not a financial one. That distinction matters, but it does not change the long-term math of investing in productive assets.”

One more thought on the midterms: with the House potentially flipping later this year and creating a split Congress, this administration is likely to pull hard on every lever it controls in the near term, including pressure on energy producers to boost output and on the Fed to loosen policy. Neither of these levers moves quickly. Oil rigs take time to mobilize; the Fed is constitutionally independent. Don’t expect political announcements to change the underlying supply picture overnight.

As always, the best portfolio is one you can hold through volatility without panic. If your allocation is giving you sleepless nights right now, that is useful information and a conversation worth having with your advisor.

DISCLOSURES:

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

This document is for your private and confidential use only and not intended for broad usage or dissemination.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of CWA strategies are disclosed in the publicly available Form ADV Part 2A.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. You cannot invest directly in an Index.

Past performance shown is not indicative of future results, which could differ substantially.

Consilio Wealth Advisors, LLC (“CWA”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where CWA and its representatives are properly licensed or exempt from licensure.